He shares valuable lessons for businesses considering a move to Singapore. The discussion explores why a growing number of Australians are choosing Singapore to expand their businesses, common misconceptions about the Singapore tax system, and the practical factors every business owner should understand before making the move.

Founded in 1992, we are an international tax and accounting firm with offices in London, New York, Los Angeles, Sydney and Singapore. With a focus on international tax, we manage the complex international tax obligation of globally mobile executives, family groups and businesses seeking to expand abroad.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Australian Businesses Expanding To The USA: Grants, Incentives and Support Programs

23rd Jun 2026

John Marcarian

The US Incentives Playbook: How Australian Businesses Can Turn Expansion Into Advantage For many Australian companies, the United States looks deceptively simple, one country, one flag, one...

Australian Businesses Expanding To The USA: What Legal Considerations Must Understand Before Expanding

26th May 2026

John Marcarian

The US Market Is Not One Market: What Australian Businesses Must Understand Before Expanding For Australian businesses with global ambition, the United States often represents the defining...

Corporate Governance And Compliance Best Practices For SMEs In Singapore

22nd May 2026

Boon Tan

Many SME owners assume that corporate governance is something reserved for listed companies, large boards and institutional investors In practice, good governance is just as important for SMEs —...

Australian Businesses Expanding To The USA: Grants, Incentives and Support Programs

John Marcarian | 23 Jun 2026 | 12 min read

The U.S. Incentives Playbook: How Australian Businesses Can Turn Expansion Into Advantage

For many Australian companies, the United States looks deceptively simple, one country, one flag, one massive consumer market.

However, the reality is far from that. Apart from culture and the use of words two other things are highly diverse as businesses move from US state to US state. The first is tax law, the second is incentives provided by governments.

America is not one market but rather a federation of federal rules, state tax systems, city-level economic development offices, local workforce programmes, utility incentives, property tax negotiations and industry-specific credits.

That complexity can often overwhelm newcomers. However, with the right planning, businesses can benefit.

The question for an Australian company should not simply be, “Where should we incorporate?” or “Which state has the lowest tax?”

The better question is – where will our U.S. activities create the most value – jobs, investment, research, manufacturing, training, clean energy or exports – and which government wants that activity enough to support it?

America Does Not Hand Out Incentives Automatically

The United States has a deep incentives ecosystem, but it is rarely automatic.

A business that signs a lease, hires staff and announces a location before speaking to the relevant economic development agencies may have already given away much of its negotiating leverage.

At the federal level, SelectUSA is a useful starting point for foreign investors.

It is led by the U.S. Department of Commerce and is designed to facilitate job-creating business investment into the United States.

It has helped facilitate more than US$400 billion in investment and supported more than 270,000 U.S. jobs, according to the Department of Commerce.

It is important to note though that SelectUSA is a gateway, not a open cheque book. While it helps investors understand the market, access data and connect with federal, state and local stakeholders – it does not itself award most state or local incentives.

This distinction matters.

In the U.S., the most valuable incentive package for an expanding business is often not a single federal grant.

It may be a carefully negotiated combination of state tax credits, local property tax abatements, workforce training support, infrastructure assistance, energy incentives and federal tax credits.

State Incentives: Where The Real Competition Begins

The U.S. states compete fiercely for investment, but they do so in different ways.

Some states emphasize low headline tax rates.

Others offer targeted credits for job creation, capital investment, research and development, advanced manufacturing, life sciences, clean energy or workforce training.

That means the “best” state is rarely the one with the lowest headline tax rate.

It is the state where the company’s operating model, workforce needs, customer base, supply chain and tax profile align.

Let’s look at New York as an example.

Its Excelsior Jobs Program can provide fully refundable tax credits over a benefit period of up to 10 years, but only where businesses meet and maintain specified job and investment thresholds.

The programme can cover credits linked to jobs, investment, research and development, real property and childcare-related expenditure.

It is attractive, but it is not automatic.

It is a performance-based programme with accountability built in.

Georgia offers a different kind of advantage through Georgia Quick Start, which provides customised workforce training free of charge to qualified new, expanding and existing businesses.

For labour-intensive or technical operations, that support can be more valuable than a headline tax credit because it directly reduces the cost and friction of building a workforce.

California’s Employment Training Panel is another example.

It provides funding to employers to assist with training that leads to long-term, well-paid jobs.

Importantly, it is a funding agency, not a training provider, so companies must still design and manage their own training strategy.

The lesson is simple – incentives follow facts.

A software company, a sports-tech platform, a medical device business and a manufacturing group may all need different states, different agencies and different applications.

Do Not Confuse “Low Tax” With “No Tax”

Australian businesses often hear that Texas and Florida are “no tax” states.

That is too simplistic.

Texas does not impose a traditional corporate income tax, but it does impose a franchise tax on taxable entities formed or organised in Texas or doing business there.

For 2026 and 2027, the Texas Comptroller lists a no-tax-due threshold of US$2.65 million and franchise tax rates of 0.375% for retail or wholesale businesses and 0.75% for other businesses, subject to the applicable rules.

Florida has no personal income tax, but that does not mean corporations operate free of state income tax.

Florida’s corporate income/franchise tax rate is 5.5% for taxable years beginning on or after 1 January 2022.

For an expanding Australian group, the state comparison should include corporate tax, franchise or gross receipts taxes, sales tax, payroll taxes, property tax, apportionment, local business taxes, employment law, labour costs, logistics, customer proximity and available incentives.

A low-tax state can still be expensive if it is the wrong commercial fit.

Zones Can Help – But Know What Kind Of Zone You Are In

Location-based incentives are common in the United States, but the terminology can be misleading. “Enterprise zone,” “opportunity zone,” “empowerment zone,” “development zone” and “distressed area” do not mean the same thing.

Opportunity Zones, for example, are frequently misunderstood.

They are primarily investor-side tax incentives.

A taxpayer may be able to defer eligible gains by investing through a Qualified Opportunity Fund, but the benefit does not operate like a direct grant to a business merely because it opens an office in a designated area.

Under current legacy rules, eligible gains invested into a Qualified Opportunity Fund may be deferred until an inclusion event or 31 December 2026, whichever is earlier.

The programme is also evolving.

IRS guidance states that the 2025 federal legislation commonly referred to as the One Big Beautiful Bill Act makes the Qualified Opportunity Zone incentive permanent, with the first post-enactment round of new QOZ designations taking effect on 1 January 2027 and new rounds following every 10 years.

It also introduced additional tax benefits for certain rural-area Opportunity Zone investments.

For practical purposes, this means a business should not simply ask, “Are we in a zone?”

It should ask: who receives the benefit, what investment is required, when must the investment be made, what compliance applies, and does the benefit fit our capital structure?

The R&D Tax Credit – Powerful, But Not A Blank Cheque

For innovative Australian companies entering the U.S., the federal R&D tax credit can be one of the most valuable incentives available.

But it is often oversold.

The U.S. R&D credit is not a reimbursement of research spending.

It is a tax credit calculated by reference to qualifying research activities and qualifying research expenses.

The activity must satisfy the section 41 requirements, including the four-part framework: the expenditure must relate to section 174-type research, the work must seek technological information, the information must be intended for use in developing a new or improved business component, and substantially all of the activity must involve a process of experimentation for a qualified purpose.

That does not mean the company must invent something never seen before.

The IRS guidance confirms there is no separate requirement that the work exceed or expand the common knowledge of skilled professionals.

In practice, the focus is on whether the company faced technical uncertainty, identified alternatives and evaluated those alternatives through a genuine process of experimentation.

Qualifying expenses are narrower than many businesses expect.

They generally include eligible wages, supplies used in qualified research, certain computer-use costs and 65% of eligible contract research expenses.

A broad claim for “cloud computing” or “software development” costs should be reviewed carefully rather than assumed to qualify automatically.

For Australian groups, one rule is especially important – foreign research does not qualify for the U.S. federal R&D credit. Research conducted outside the United States, Puerto Rico or U.S. possessions is excluded, even if it is performed for a U.S. taxpayer or by American researchers.

That means work performed by engineers in Sydney, Melbourne or Brisbane generally cannot be converted into a U.S. federal R&D credit merely because the intellectual property is later used by a U.S. subsidiary.

The structure of contracts, ownership of IP, location of personnel, funding arrangements and technical records all matter.

The Payroll Tax Opportunity For Younger Companies

For early-stage businesses, the R&D credit may be valuable even before the company has meaningful income tax liability.

A qualified small business may elect to use up to US$500,000 of its research credit against payroll tax for tax years beginning after 31 December 2022.

The IRS states that the payroll tax credit is first used against the employer share of Social Security tax, with remaining credit then reducing the employer share of Medicare tax for the quarter.

The eligibility rules are specific.

A qualified small business generally must have gross receipts of less than US$5 million for the tax year and no gross receipts for any tax year before the five-tax-year period ending with the credit year.

The election is also subject to timing and repeat-use limits.

For a young Australian technology company launching in the U.S., that can be meaningful cash-flow support.

But the company needs the right records from day one: project descriptions, technical uncertainties, employee time allocation, contracts, invoices and evidence of experimentation.

Do Not Confuse The R&D Credit With R&E Expensing

Another common trap is mixing up the R&D credit with the deduction rules for research and experimental expenditure.

Following recent U.S. tax changes, taxpayers may generally deduct domestic research or experimental expenditure paid or incurred in taxable years beginning after 31 December 2024, or elect to capitalise and amortise those domestic costs over at least 60 months.

Foreign research or experimental expenditure cannot be currently deducted and is generally amortised over 15 years.

That distinction is important for cross-border planning.

A U.S. subsidiary carrying out domestic research may have both credit and deduction considerations.

An Australian parent carrying out research offshore may face a different U.S. outcome.

For groups with shared development teams, intercompany agreements and transfer pricing policies should be aligned with the intended tax position.

Clean Energy Incentives – Attractive, But Increasingly Technical

Sustainability incentives remain significant, but the rules are now highly technical.

The U.S. Clean Electricity Investment Credit has a base credit amount of 6% of qualified investment.

That amount can increase up to 30% where prevailing wage and registered apprenticeship requirements are satisfied.

Additional 10-percentage-point bonuses may be available for projects meeting certain domestic content requirements or located in an energy community.

The credit may also be eligible for direct payment or transferability in certain circumstances, although taxpayers cannot claim both the investment credit and production credit for the same facility.

This is a major planning area for businesses investing in solar, storage, clean electricity, manufacturing facilities or energy-intensive operations.

But the “30% credit” should not be described as automatic.

It depends on the project, the property, labour compliance, timing, location, domestic content, tax ownership and documentation.

The timing rules are also changing.

IRS Notice 2025-42 explains that, under the 2025 legislation, section 45Y and section 48E credits terminate for applicable wind and solar facilities placed in service after 31 December 2027 where construction begins after 4 July 2026.

For businesses, the message is clear – clean energy tax credits can improve project economics, but they should be modelled before committing capital.

A rooftop solar project, a battery installation, a manufacturing upgrade and a major renewable generation project may all sit under different rules.

The Real Strategy – Design The U.S. Footprint Before Asking For Incentives

The most successful incentive strategies are built before the U.S. expansion is announced.

Once a company has chosen a state, signed a lease, hired staff and committed publicly, the economic development agency may have little reason to offer support.

A strong U.S. incentives review should ask:

What activities will be performed in the U.S.?

How many jobs will be created, and at what wage level?

What capital expenditure will be made?

Will the company conduct U.S.-based R&D?

Will it invest in training, manufacturing, clean energy, logistics or distressed-area development?

Does the company need incentives as cash grants, tax credits, abatements, training support or infrastructure assistance?

Are the incentives discretionary, automatic, refundable, transferable or subject to clawback?

How will the structure interact with Australian tax, U.S. federal tax, state tax and transfer pricing?

The businesses that win do not treat incentives as an afterthought.

They treat them as part of site selection, entity structuring, workforce planning and capital allocation.

Final Word – America Rewards Specificity

The U.S. incentive system is not simple but it can be worked through.

Australian businesses should avoid three mistakes:

assuming incentives are automatic;

chasing headline tax rates without modelling the full operating cost; and

trying to claim credits after the commercial facts have already been locked in.

The better approach is to enter the U.S. with a clear operating story, where the company will invest, who it will hire, what it will build, what technology it will develop and how its presence will benefit the local economy.

In America, governments do not usually subsidise vague ambition.

They support specific activity.

The companies that understand that early can turn U.S. expansion from a cost centre into a strategic advantage.

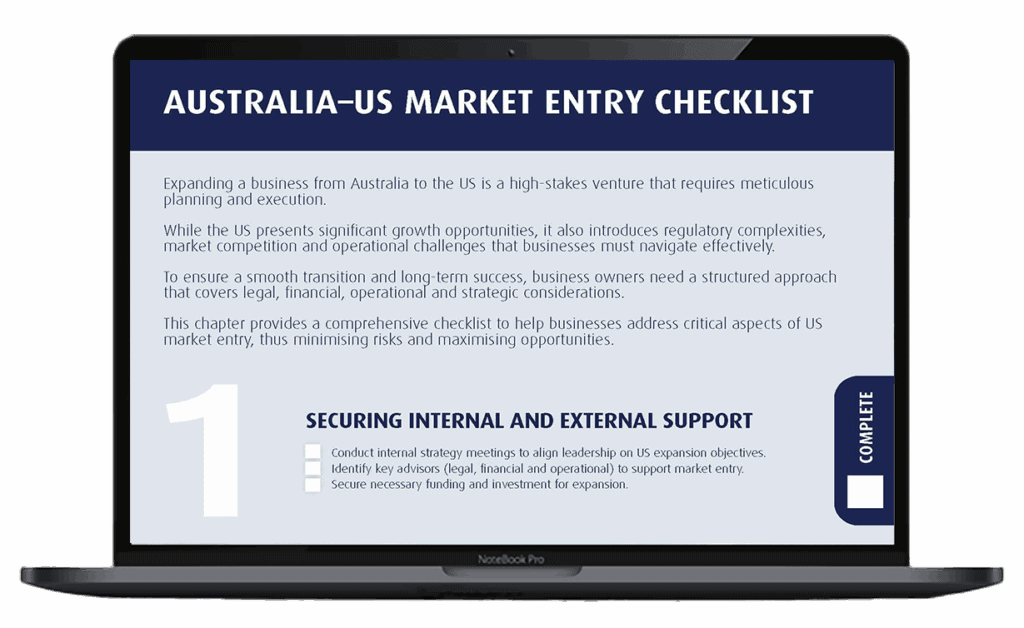

CHECKLIST: Australia – US Market Entry Checklist

To assist you and your team we have created the “Australia-US Market Entry Checklist“. The checklist guides your team through:

Identifying the most appropriate and strategic pathways for US expansion by Australian businesses.

Reducing expansion risk through clear tax, legal, and regulatory guidance.

Enabling a smooth transition into the US market and maximising long-term success.

Written by John Marcarian

John is an Australian Chartered Accountant with over 25 years of experience.

Having founded CST Tax Advisors in 1992, John has in-depth knowledge of international tax matters for both businesses and globally mobile expats.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Podcast: What A $4B Company Taught Us About Moving To Singapore

25th Jul 2026

CST Tax Advisors

Our Managing Director in Singapore, Boon Tan, recently joined Tim Raes and Jamie Bergman, hosts of the podcast Aussie Expat In the episode What A $4B Company Taught Us About Moving To...

Australian Businesses Expanding To The USA: What Legal Considerations Must Understand Before Expanding

26th May 2026

John Marcarian

The US Market Is Not One Market: What Australian Businesses Must Understand Before Expanding For Australian businesses with global ambition, the United States often represents the defining...

Corporate Governance And Compliance Best Practices For SMEs In Singapore

22nd May 2026

Boon Tan

Many SME owners assume that corporate governance is something reserved for listed companies, large boards and institutional investors In practice, good governance is just as important for SMEs —...

Australian Businesses Expanding To The USA: What Legal Considerations Must Understand Before Expanding

John Marcarian | 26 May 2026 | 17 min read

The US Market Is Not One Market: What Australian Businesses Must Understand Before Expanding

For Australian businesses with global ambition, the United States often represents the defining opportunity.

It is the world’s largest consumer market, one of the deepest capital markets, and home to many of the customers, investors, strategic partners and industry ecosystems that can transform a company’s trajectory. For businesses in technology, sport, health, consumer products, professional services, education, financial services and advanced manufacturing, the US is often not simply an expansion market. It is the market that determines whether the business becomes regional or genuinely global.

Yet the same qualities that make the US attractive also make it unforgiving.

Australian businesses often approach the US with a degree of familiarity. The language is familiar. The legal heritage feels familiar. The commercial culture is recognisable. The brands, investors and institutions are globally known. On the surface, the US can appear to be a larger version of a market Australian businesses already understand.

That assumption is dangerous.

The United States is not just a bigger market. It is a different legal, tax and regulatory environment altogether. More importantly, it is not one market in any simple sense. It is a federation of states, cities, regulators, courts and commercial norms layered on top of a federal system. A business may enter through California, raise capital in Delaware, hire in New York, sell into Texas, store data in Virginia and use contractors in Florida — and each of those choices can carry different legal and commercial consequences.

This is where many Australian businesses underestimate the challenge. They do not fail because the US opportunity is too difficult. They fail because they treat US expansion as a sales project when it is also a structural, legal, tax and governance project.

The distinction matters.

A company that enters the US with the wrong structure, weak contracts, unprotected intellectual property, inadequate insurance, poor employment processes or unmanaged privacy exposure may still generate revenue. It may even grow quickly. But growth without structure can simply scale the risk. By the time the issue appears — an investor diligence request, a lawsuit, a tax notice, a product complaint, a data incident, a distributor dispute or a regulatory inquiry — the cost of fixing the problem is usually far greater than the cost of preparing properly at the outset.

Structure Is A Strategic Decision, Not An Administrative Step

The first serious question for an Australian business entering the US is not where to sell, but how to exist in the market.

Should the business operate directly from Australia? Should it form a US subsidiary? Should that subsidiary be a corporation or an LLC? Should it be established in Delaware, the state of operation, or somewhere else? Should the group structure be reorganised before a US capital raise? Should intellectual property remain in Australia or be licensed to the US entity? How should intercompany arrangements be documented?

These questions are often treated as technical matters. They are not. They influence tax outcomes, investor appetite, legal liability, operating flexibility, employee equity arrangements, state filing obligations, exit planning and the perceived maturity of the business.

For many Australian companies, a US subsidiary can be a sensible way to separate US operating risk from the Australian parent. But that protection is not automatic. A subsidiary is not a piece of paper that magically insulates the group from all exposure. It must be respected as a real entity. That means separate accounts, proper contracts, appropriate capitalisation, clear decision-making, arm’s-length intercompany arrangements and disciplined corporate governance.

Where the business is a high-growth startup seeking US venture capital, a different issue may arise. US investors, particularly venture funds, often prefer investing into a US parent company, commonly a Delaware corporation. This can lead to a “flip-up”, where the corporate structure is reorganised so that the US company becomes the parent of the group.

For the right business, this may be commercially sensible. It can align the structure with US investor expectations, simplify future funding rounds and position the company for a US exit. But it should never be treated as a cosmetic change. A flip-up can have consequences for Australian tax, US tax, shareholders, employee equity plans, intellectual property ownership and future exit proceeds. It is one of those decisions that looks simple only when viewed from too far away.

The broader point is that structure should follow strategy. A founder-led software company preparing for US venture capital does not necessarily need the same structure as an Australian manufacturer selling through US distributors. A professional services firm establishing a US client base has different issues again. A sports, entertainment or talent-related business may need to think carefully about immigration, state law, withholding, image rights, contracting and agency arrangements.

The correct structure is not the most popular one. It is the one that supports the commercial plan while managing tax, legal and operational risk.

Contracts Are The Operating System Of US Risk

In the US, contracts carry more weight than many Australian businesses expect.

A contract is not merely a record of what the parties agreed. It is a risk allocation tool. It determines who bears responsibility if something goes wrong, whether liability is capped, whether consequential damages are excluded, who owns the intellectual property, how confidential information is protected, which law applies, where disputes are heard, whether arbitration is required, whether legal costs can be recovered and what happens when the relationship breaks down.

This matters because the US litigation environment is expensive. Discovery can be broad and intrusive. Legal fees can escalate quickly. Claims that appear commercially manageable can become financially distracting. Even a strong defence can consume executive time, damage relationships and create pressure to settle.

Australian businesses should therefore treat US contracts as a commercial control system, not as administrative paperwork.

The key clauses are not boilerplate. Indemnities, warranties, limitations of liability, governing law, jurisdiction, dispute resolution, confidentiality, IP ownership, non-solicitation, termination, payment terms, audit rights and insurance obligations all need to be drafted for the transaction and the relevant US context.

This is also where businesses need to be cautious about relying on AI-generated documents or generic templates.

The issue is not that AI has no role. It can be useful for early drafting, issue spotting and helping business owners understand common contractual concepts. The problem is that a contract can sound sophisticated and still be wrong. It can use terminology that appears legal but does not achieve the intended result. It can import concepts from the wrong jurisdiction. It can omit state-specific requirements. It can include a clause that is unenforceable, commercially unrealistic or unsuitable for the industry.

In the US, the difference between a contract that looks right and a contract that works can be very expensive.

Intellectual Property Should Be Protected Before The Business Becomes Visible

For many Australian companies, the most valuable assets entering the US are not physical assets. They are brands, software, product designs, proprietary processes, client data, trade secrets, content, know-how, commercial relationships and reputation.

Those assets need to be protected before the business becomes visible.

Too many companies reverse the sequence. They launch the product, appoint a distributor, speak to investors, hire contractors, share technical information, run a campaign, build a customer base and only then ask whether their intellectual property is protected in the US. By that stage, the business may discover that a similar brand is already registered, a contractor agreement does not properly assign IP, confidential information has been shared too broadly, or a competitor has moved faster.

In the US, trade marks, patents, copyright and trade secrets each require different thinking.

A brand that is available in Australia may not be available in the US. A name that feels distinctive to an Australian founder may already be used by a US company in a related category. A trade mark search and filing strategy should therefore be addressed early, particularly where the US brand will be central to market entry.

For technology and product businesses, patent timing can be critical. Public disclosure, investor presentations, product launches and commercial negotiations can all affect the position if not managed properly. Businesses with potentially patentable technology should obtain advice before they disclose too much.

For software, content and creative assets, copyright protection may be important, but businesses should also ensure that ownership is clean. That means reviewing agreements with developers, agencies, consultants, employees and contractors. It is surprisingly common for companies to assume they own what they paid to create, only to find the legal position is more complicated.

Trade secrets require discipline. Confidential information is not protected merely because the business considers it confidential. Protection depends on practical steps: non-disclosure agreements, access controls, internal policies, employee obligations, contractor restrictions, cybersecurity practices and careful management of commercial discussions.

The principle is simple. If the US market is important enough to enter, the assets being taken into that market are important enough to protect.

Product Liability And Consumer Risk Can Change The Economics Of Expansion

For businesses selling physical products, the US requires particular care.

The US product liability environment can be far more aggressive than Australian businesses expect. Claims may arise from alleged design defects, manufacturing defects, inadequate warnings, poor instructions, breach of warranty, misleading marketing or failure to act once a product risk becomes known. Manufacturers, distributors and retailers can all be drawn into disputes, even where the business believes it acted responsibly.

This can be especially confronting for Australian companies that have strong internal quality standards and assume those standards will be enough. In the US, the question is not only whether the product was made carefully. It is also whether the design was appropriate, whether foreseeable misuse was considered, whether warnings were adequate, whether instructions were clear, whether claims made in marketing were supportable, whether warranties were properly drafted and whether the company had systems to respond to complaints or safety issues.

Before entering the US, product businesses should review packaging, warnings, instructions, safety certifications, warranties, recall procedures, supply chain contracts, distributor obligations and insurance coverage. The insurance point is critical. Australian policies may not provide the protection required for US exposure, or may contain territorial exclusions, product exclusions or limits that are inadequate for the US market.

A business should not ask only whether it can sell the product in the US. It should ask whether it is prepared for the legal consequences of selling the product in the US.

Compliance Is Fragmented, And Fragmentation Creates Risk

One of the defining features of the US market is regulatory fragmentation.

There are federal regulators, state regulators and local authorities. There are national rules, state-specific rules and city-level requirements. There are industry-specific regimes and general consumer laws. There are licensing rules, employment rules, tax rules, privacy rules, advertising rules, import rules and product safety rules.

The relevant obligations depend heavily on what the business does.

A food, cosmetics, health, medical device or pharmaceutical business may need to consider FDA requirements. A financial services or investment-related business may need to consider securities regulation. A company making environmental claims may need to substantiate those claims carefully. A consumer product business may need to consider product safety standards. An online business may need to consider privacy, automatic renewal rules, digital marketing obligations and state consumer protection laws. A business importing goods may need to consider customs, tariffs, sanctions and restricted-party screening.

This is why there is no single US compliance checklist that works for every Australian business. The right analysis depends on the product or service, the states involved, the customer base, the distribution model, the industry and the way the business earns revenue.

The problem is that many compliance risks arise before the company thinks it has “entered” the US in a formal sense. A business may create US exposure by selling online to US customers, engaging US influencers, collecting data from US residents, appointing a US sales agent, attending trade shows, hiring contractors, storing inventory, using a fulfilment provider or raising capital from US investors.

Market entry is not always marked by opening an office. Sometimes it begins with the first US customer.

Marketing, Privacy And Data Practices Need To Be US-Ready

The US is a powerful market for digital growth, but it is also a market where marketing practices, consumer disclosures and data handling can create significant risk.

Advertising must be accurate. Performance claims need support. Pricing needs to be clear. Promotional terms need to be properly disclosed. Influencer relationships need to be transparent. Subscription arrangements and automatic renewals need careful attention. Environmental claims, health claims and financial claims require particular care because they can attract scrutiny if they are exaggerated, vague or insufficiently substantiated.

This matters for Australian businesses because many enter the US digitally. They sell through a website, run paid advertising, use influencers, collect customer information, offer subscriptions, promote through social media and sell across multiple states before building a physical presence.

That model can scale quickly. It can also scale legal exposure quickly.

Privacy is another area where Australian assumptions can be misleading. The US does not operate under one simple, comprehensive national privacy regime that applies uniformly to every business. Instead, it has a patchwork of state privacy laws, federal sector-specific laws, breach notification obligations and industry-specific requirements.

California is often the best-known example, but it is not the only state that matters. Health data, children’s data, biometric information, financial information and sensitive personal information may carry additional obligations depending on how the business operates.

Privacy should therefore be treated as an operational issue, not merely a website policy issue. Businesses need to know what information they collect, why they collect it, where it is stored, who receives it, how long it is retained, how it is protected and what rights customers may have.

A privacy policy that looks acceptable on a website is not enough if the underlying systems do not match it.

Governance Protects The Business When Growth Accelerates

In early-stage expansion, governance often feels secondary to sales. That is understandable, but it is also risky.

A company entering the US needs basic corporate discipline. It should maintain proper records, document key decisions, separate group entities, keep accurate accounts, ensure contracts are signed by the correct entity, manage tax registrations, comply with employment obligations and maintain appropriate insurance.

This is not bureaucracy for its own sake. It is what protects the business when pressure arrives.

If a dispute arises, the company’s documents matter. If an investor conducts due diligence, the records matter. If a regulator asks questions, the systems matter. If a customer makes a claim, the contract and insurance position matter. If the business is eventually sold, the buyer will examine whether the US operations were built properly or improvised.

Poor governance can also create personal exposure for executives in certain circumstances, particularly where there are unpaid taxes, employment law breaches, personal guarantees, fraud, misuse of entities, commingling of funds or serious compliance failures. While corporate structures can provide important protection, they are not a substitute for responsible management.

Insurance is part of this framework. Depending on the business, relevant policies may include general liability, product liability, cyber, directors and officers, employment practices liability, professional liability and workers’ compensation. But insurance should not be treated as a cure-all. Coverage depends on policy wording, exclusions, limits, retentions, notification requirements and the nature of the claim.

Good governance does not slow growth. Done properly, it makes growth more durable.

The Businesses That Succeed Prepare Before The Market Tests Them

The US rewards ambition, but it also tests assumptions.

Australian businesses that succeed in the US usually understand that expansion is not a single event. It is a sequence of decisions that must fit together: structure, tax, contracts, IP, employment, privacy, insurance, regulatory compliance, financing and governance. None of these issues should be considered in isolation because each one affects the others.

The businesses that struggle often follow a familiar pattern. They sell first and structure later. They use Australian contracts in US transactions. They assume a template agreement will be sufficient. They leave IP protection until after launch. They hire contractors without understanding worker classification. They underestimate state taxes and sales tax. They use marketing claims that have not been reviewed. They collect data without mapping their obligations. They discover insurance gaps only after a claim.

None of these mistakes necessarily comes from carelessness. More often, they come from momentum. The company sees an opportunity, moves quickly, wins customers and assumes the infrastructure can catch up later.

In the US, that can be an expensive assumption.

The better approach is not to over-lawyer the opportunity or delay commercial progress. The better approach is to build a practical expansion framework before the business is exposed. That means identifying the highest-risk issues early, prioritising what must be fixed before launch, and creating a structure that can evolve as the US business grows.

A business entering the US does not need perfection from day one. But it does need clarity. It needs to know which entity is contracting, who owns the IP, what taxes may apply, which states matter, what the contracts say, what insurance covers, what employment obligations exist, what data is collected and what regulatory regimes are relevant.

That clarity gives management the confidence to grow without constantly discovering hidden risk.

The Real Opportunity Is Building A US Platform, Not Just Making US Sales

The US can be transformational for Australian businesses. It can provide access to capital, customers, strategic partners, talent, acquirers and industry ecosystems that are difficult to replicate elsewhere.

But the businesses that create lasting value in the US do more than make sales. They build a platform.

A platform has the right structure. It has contracts that allocate risk properly. It protects intellectual property. It understands its tax position. It has employment and contractor processes. It manages privacy and data. It has suitable insurance. It complies with relevant regulation. It keeps records. It can withstand investor diligence, customer scrutiny, regulator questions and commercial disputes.

That is the difference between entering the US and being ready for the US.

For Australian businesses, the message is not that the US is too complex. Complexity is manageable. The real issue is whether the business recognises the complexity early enough to turn it into a competitive advantage.

A well-structured Australian business can enter the US with confidence. It can move faster because the major risks have been considered. It can negotiate better because its contracts are prepared. It can raise capital more effectively because its structure makes sense. It can protect value because its IP is secured. It can respond to disputes because its documents and insurance are in order.

US expansion should not be approached with fear. It should be approached with discipline.

The companies that do this well will not see legal, tax and compliance planning as obstacles to growth. They will see them as part of the architecture of growth.

Because in the US, getting to market is only the first challenge.

The real test is whether the business has been built to survive success.

CHECKLIST: Australia – US Market Entry Checklist

To assist you and your team we have created the “Australia-US Market Entry Checklist“. The checklist guides your team through:

Identifying the most appropriate and strategic pathways for US expansion by Australian businesses.

Reducing expansion risk through clear tax, legal, and regulatory guidance.

Enabling a smooth transition into the US market and maximising long-term success.

Written by John Marcarian

John is an Australian Chartered Accountant with over 25 years of experience.

Having founded CST Tax Advisors in 1992, John has in-depth knowledge of international tax matters for both businesses and globally mobile expats.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Podcast: What A $4B Company Taught Us About Moving To Singapore

25th Jul 2026

CST Tax Advisors

Our Managing Director in Singapore, Boon Tan, recently joined Tim Raes and Jamie Bergman, hosts of the podcast Aussie Expat In the episode What A $4B Company Taught Us About Moving To...

Australian Businesses Expanding To The USA: Grants, Incentives and Support Programs

23rd Jun 2026

John Marcarian

The US Incentives Playbook: How Australian Businesses Can Turn Expansion Into Advantage For many Australian companies, the United States looks deceptively simple, one country, one flag, one...

Corporate Governance And Compliance Best Practices For SMEs In Singapore

22nd May 2026

Boon Tan

Many SME owners assume that corporate governance is something reserved for listed companies, large boards and institutional investors In practice, good governance is just as important for SMEs —...

Corporate Governance And Compliance Best Practices For SMEs In Singapore

Boon Tan | 22 May 2026 | 7 min read

Many SME owners assume that corporate governance is something reserved for listed companies, large boards and institutional investors. In practice, good governance is just as important for SMEs — and often more straightforward to implement. It is about having clear decision-making, accurate records, timely filings, strong financial controls and a business culture that reduces risk.

In Singapore, governance and compliance are not merely administrative obligations. They help SMEs build credibility with banks, investors, suppliers, customers and government agencies. They also reduce the risk of penalties, disputes and operational disruption. For growing businesses, good governance can also make expansion, fundraising and succession planning easier to manage.

From my experience in Singapore, failure to implement a governance framework can lead to compliance failures, such as failing to lodge a report on time, meaning financial penalties. In extreme cases, I have also seen statutory records not reflecting the commercial position the company is operating under.

1. Start With Director Accountability

In many SMEs, the directors are also the founders, shareholders and day-to-day managers. This overlap can speed up decision-making, but it can also blur the line between ownership and stewardship.

The corporate regulator, ACRA, highlights that directors remain legally responsible for the company’s affairs, even where tasks are delegated to management, finance teams, corporate secretaries or tax agents.

With effect from May 2026, heavier penalties apply for directors who breach duties such as failing to act in the company’s best interests or to exercise reasonable diligence. Maximum fines have increased from S$5,000 to S$20,000, and serious offences may involve both fines and imprisonment of up to 12 months.

For SME directors, “reasonable diligence” can include practical steps such as regularly reviewing management reports, understanding major contracts before approval, ensuring tax and regulatory filings are completed on time, and asking questions when financial or operational issues arise.

A practical starting point is to maintain a simple “reserved matters” list. This should identify decisions that require unanimous approval by directors or shareholders, such as taking on significant debt, issuing shares, approving major contracts, entering into related-party transactions, opening overseas entities, changing key bank mandates, or approving dividends.

2. Build A Compliance Calendar Around The Financial Year-End

SMEs should maintain a compliance calendar that works backwards from the company’s financial year-end, to ensure the key compliance due dates are not missed.

Some important deadlines include:

Annual general meetings (AGM): Non-listed Singapore companies must hold their AGM within six months after the financial year-end, unless exempt or the AGM has been properly dispensed with.

Annual returns: All Singapore companies, including inactive or dormant companies, must file annual returns with ACRA. The filing deadline is generally within 7 months of the financial year-end.

Company secretary appointment: A licensed company secretary must be appointed within six months of registration.

Auditor appointment: An auditor must be appointed within three months of incorporation unless the company qualifies for an audit exemption. For reference, the small company exemption applies when a private company meets two of the following three conditions: revenue ≤ S$10m, assets ≤ S$10m, and employees ≤ 50.

3. Keep Statutory Registers And Ownership Records Current

Good governance requires accurate records of who owns, controls and manages the company. Any changes to officers and shareholders must be reported within 14 days to avoid late lodgement penalties.

Companies should also pay attention to beneficial ownership and nominee arrangements to ensure compliance with the Register of Registrable Controllers requirements.

4. Treat Tax Compliance As A Governance Matter

Tax compliance should not be viewed as a purely accounting function. It is a governance issue because directors remain responsible for ensuring filings are timely and accurate.

I have discussed tax compliance in the past, but a quick summary is as follows:

Income Tax

The Estimated Chargeable Income (ECI) return is due within three months from the end of their financial year, unless they qualify for an ECI filing waiver or are specifically not required to file.

The corporate income tax return is due by 30 November each year unless a waiver applies.

Directors remain responsible for timely and accurate filing even when a tax agent has been engaged, and late filing or non-filing may result in penalties of up to S$5,000 if directors continually fail to manage their compliance obligations.

GST

A business must register for GST if its taxable turnover is more than S$1 million under the retrospective view at the end of the calendar year, or if it is expected to be more than S$1 million in the next 12 months under the prospective view.

Businesses should also monitor the GST InvoiceNow requirement. IRAS states that GST-registered businesses are required to use InvoiceNow-ready solutions to transmit invoice data directly to IRAS, with phased implementation beginning from 1 November 2025 for certain newly incorporated companies applying for voluntary GST registration, and from 1 April 2026 for all businesses applying for new voluntary GST registration.

At the Committee of Supply 2026, the Government further announced that all remaining GST-registered businesses will be required to onboard InvoiceNow progressively between April 2028 and April 2031, with transitional grants of up to S$1,000 for SMEs.

Transfer Pricing

SMEs with cross-border related-party transactions must comply with the arm’s length principle when transacting with related parties and maintain contemporaneous transfer pricing documentation to substantiate their pricing where relevant.

5. Manage Employment, Payroll And CPF Obligations Carefully

SMEs should maintain proper employment records, issue itemised payslips, process CPF contributions on time, and ensure employment terms are clearly documented.

The Ministry of Manpower (MOM) states that employers must maintain records for all employees covered by the Employment Act. For current employees, employers must keep the most recent 2 years of records. For former employees, the last two years of records must be retained for one year after the employee leaves.

CPF contributions are due on the last day of the calendar month. In addition to late-payment interest, enforcement action may be taken if employers repeatedly fail to pay by the due date.

6. Put Data Protection And Cybersecurity On The Agenda

Most SMEs now collect personal data through customer forms, websites, e-commerce platforms, HR records, marketing campaigns or supplier databases. Data protection is therefore a core governance issue.

Under the Personal Data Protection Act, organisations must appoint a Data Protection Officer (DPO) and make the DPO’s contact information publicly available.

SMEs should not wait for a data incident before assigning responsibility for data protection. Practical steps include maintaining a personal data inventory, limiting access rights, reviewing vendor contracts, training staff, implementing password and access controls, and preparing a data breach response plan.

7. Make Governance Proportionate, Practical And Repeatable

A SME governance framework should be practical, scalable and easy to maintain. Good governance in key areas should include:

Corporate Compliance

A compliance calendar tied to the financial year-end

Clear director and shareholder approval thresholds

Accurate statutory registers and ownership records

Financial And Tax Controls

Monthly financial reporting and bank reconciliations

Documented tax, GST and transfer pricing processes

Employment And Payroll

Proper employment records and itemised payslips

Clear payroll and CPF procedures

Data Protection And Operations

A basic data protection management process

Regular review with corporate secretarial, tax and accounting advisers

Good governance is ultimately about discipline. It helps SMEs make better decisions, protect value, reduce regulatory risk and build trust with stakeholders.

In Singapore’s competitive business environment, SMEs that invest early in governance and compliance are better positioned to scale sustainably and confidently. If you’d like to discuss how any of this applies to your business, feel free to reach out.

Written by Boon Tan

Australian born with Singaporean heritage, Boon provides specialist tax advice to our clients in relation to establishment of corporate structures in Singapore and in-bound/out-bound taxation matters for individuals including expatriate employee and founders of companies entering Singapore.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Podcast: What A $4B Company Taught Us About Moving To Singapore

25th Jul 2026

CST Tax Advisors

Our Managing Director in Singapore, Boon Tan, recently joined Tim Raes and Jamie Bergman, hosts of the podcast Aussie Expat In the episode What A $4B Company Taught Us About Moving To...

Australian Businesses Expanding To The USA: Grants, Incentives and Support Programs

23rd Jun 2026

John Marcarian

The US Incentives Playbook: How Australian Businesses Can Turn Expansion Into Advantage For many Australian companies, the United States looks deceptively simple, one country, one flag, one...

Australian Businesses Expanding To The USA: What Legal Considerations Must Understand Before Expanding

26th May 2026

John Marcarian

The US Market Is Not One Market: What Australian Businesses Must Understand Before Expanding For Australian businesses with global ambition, the United States often represents the defining...

Businesses Expanding Into Singapore Must Commit Meaningful Time And Capital To Achieve Market Entry Success

Boon Tan | 21 Apr 2026 | 3 min read

Singapore remains one of the most attractive global hubs for business expansion — politically stable, legally transparent, financially robust, and strategically positioned at the heart of Southeast Asia.

Yet a persistent misconception — particularly among first-time entrants — is that setting up in Singapore is little more than an administrative exercise.

Incorporation can indeed be completed quickly. Successful market entry cannot.

In my practice, I have seen three dimensions that consistently separate the companies that thrive here from those that stall.

1. Time – Building Credibility And Commercial Traction

Singapore, like much of Asia, is a relationship-driven market operating within a highly structured regulatory framework. Whether engaging with banks, regulators, counterparties, or talent, credibility is not assumed — it is earned over time.

New entrants often underestimate how long it takes to:

Establish robust banking relationships in an increasingly strict compliance environment

Build trust with local partners, customers, and suppliers

Navigate regulatory expectations across sectors such as financial services, trading, and technology

This does not mean hiring on day one. It means being physically present in Singapore — meeting potential customers, partners, and suppliers, and laying the foundation for what comes next. Businesses that succeed here are those prepared to invest the time to build a durable, credible presence.

Bank Account Opening

Banking is a prime illustration. The standard timeframe to open a corporate account in Singapore is 6 – 8 weeks, driven by the compliance rigour around KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements.

Banks place significant weight on understanding who they are dealing with. Applications must be supported with full identification of officeholders, shareholders, and ultimate beneficial owners, plus an overview of the business, projected transaction levels and values, and details of your customers and suppliers.

Plan for it — and start early.

2. Capital – Beyond The Statutory Minimum

Statutory share capital thresholds in Singapore are low. The practical capital required to succeed here is anything but.

The share capital you inject into your Singapore company signals to the market — and to regulators — how serious you are about building a presence.

Companies should be prepared to fund:

Initial operating costs and runway of at least 12 – 24 months

Experienced local or regional talent

Compliance, governance, and reporting infrastructure

Office space, technology systems, and operational support

Under-capitalisation is one of the most common reasons market entry stalls or fails. Singapore rewards well-funded, well-prepared businesses that demonstrate long-term commitment.

A Tangible Example: When applying for an Employment Pass for an expatriate hire, the Ministry of Manpower assesses the application in part against the paid-up share capital of the sponsoring company. Thin capitalisation, thin chances.

3. Local Execution – Adapting Strategy To The Market

Strategies that succeed in Europe, the US, or elsewhere in Asia do not always translate directly into Singapore.

Effective execution requires:

Alignment with Singapore’s regulatory and tax frameworks

Understanding of local business culture and decision-making norms

Tailoring of products, pricing, and go-to-market strategies for the regional customer base

In many cases, this means rethinking — not simply replicating — the existing business model.

A Strategic Investment, Not An Administrative Step

Singapore offers outstanding opportunities for growth, but it is not a passive or frictionless market. Entry should be treated as a strategic investment — one that demands thoughtful planning, adequate resourcing, and long-term commitment.

The businesses that succeed here are not the fastest to enter. They are the best prepared to stay, scale, and integrate into the ecosystem.

Written by Boon Tan

Australian born with Singaporean heritage, Boon provides specialist tax advice to our clients in relation to establishment of corporate structures in Singapore and in-bound/out-bound taxation matters for individuals including expatriate employee and founders of companies entering Singapore.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Podcast: What A $4B Company Taught Us About Moving To Singapore

25th Jul 2026

CST Tax Advisors

Our Managing Director in Singapore, Boon Tan, recently joined Tim Raes and Jamie Bergman, hosts of the podcast Aussie Expat In the episode What A $4B Company Taught Us About Moving To...

Australian Businesses Expanding To The USA: Grants, Incentives and Support Programs

23rd Jun 2026

John Marcarian

The US Incentives Playbook: How Australian Businesses Can Turn Expansion Into Advantage For many Australian companies, the United States looks deceptively simple, one country, one flag, one...

Australian Businesses Expanding To The USA: What Legal Considerations Must Understand Before Expanding

26th May 2026

John Marcarian

The US Market Is Not One Market: What Australian Businesses Must Understand Before Expanding For Australian businesses with global ambition, the United States often represents the defining...

Expanding Into The US? Australian Businesses Need More Than A Good Strategy — They Need A Clean Reporting Foundation

John Marcarian | 15 Apr 2026 | 4 min read

When Australian business owners talk to me about entering the US, the conversation usually starts where it should – growth.

A bigger market, deeper capital, more customers, stronger partnerships.

The opportunity is real. What is often underestimated, though, is how quickly momentum can slow due to tax and reporting issues that were never properly mapped at the start. In the US, you are rarely dealing with one simple compliance system. Federal rules are only part of the picture. State tax, registration and sales tax obligations can arrive much earlier than many businesses expect.

One of the first things I usually encourage clients to think through carefully is the entity itself.

Too often, the structure is treated as something that can be tidied up later. In practice, that can be an expensive mistake. A C corporation files Form 1120 and is taxed separately. A partnership files Form 1065 and pushes tax items out to the owners through Schedule K-1. A single-member LLC is generally disregarded for US income tax purposes unless it elects to be taxed as a corporation. On paper that may sound technical, but commercially it matters a great deal, because the wrong structure can create complexity long before the business has properly found its feet.

If an Australian group is looking at a US LLC, I would be especially careful. Where a foreign-owned US disregarded entity has reportable related-party transactions, Form 5472 can come into play, and it is filed with a pro forma Form 1120. The penalty for missing that filing starts at $25,000. That is exactly the kind of issue that catches decent businesses off guard—not because they are doing anything aggressive, but because nobody warned them early enough that the reporting obligation existed in the first place.

The state-tax piece is where many founders realise that the US is less one market and more fifty overlapping systems. Sales tax, state income tax, franchise tax and registration obligations can arise in different ways and at different times. Even the “business-friendly state” conversation needs a bit of nuance. Texas has franchise tax, Florida has corporate income/franchise tax, and many states now apply economic nexus rules that can pull remote sellers into registration and collection once thresholds are met.

Financial reporting deserves a little more attention than it usually gets at the start as well. In a public company context, SEC reporting can mean ongoing Form 10-K and Form 10-Q filings. More broadly, US financial reporting still revolves around GAAP. In practice, the challenge is often not understanding the theory, but ensuring the US numbers can be reported cleanly and consistently within the wider group without constant rework.

Hiring in the US is another area where practical business decisions and compliance meet very quickly. Employers generally need to withhold federal income tax and Social Security and Medicare taxes from wages, and most employers also need to deal with unemployment taxes at both federal and state levels. On top of that, worker classification matters. The IRS looks at the full relationship and the degree of control, not just what the contract happens to call someone. That is why I always say that calling a person a contractor is not the same thing as them actually being one.

Once the US business starts moving money across borders, the international rules need to be treated seriously. US persons with foreign financial accounts may have an FBAR filing obligation once aggregate balances exceed $10,000, and intercompany charges between an Australian parent and a US operation need to satisfy the arm’s-length standard. The best time to think about that is before the structure goes live, not halfway through an audit trail reconstruction exercise.

The good news is that none of this is unmanageable.

But it does reward businesses that treat tax and financial reporting as part of commercial strategy, rather than as admin to be cleaned up later.

The businesses that usually do well in the US are not always the ones that move fastest. They are often the ones that enter with the clearest structure, the best discipline and the fewest surprises. In my experience, that is where good advice still pays for itself.

CHECKLIST: Australia – US Market Entry Checklist

To assist you and your team we have created the “Australia-US Market Entry Checklist“. The checklist guides your team through:

Identifying the most appropriate and strategic pathways for US expansion by Australian businesses.

Reducing expansion risk through clear tax, legal, and regulatory guidance.

Enabling a smooth transition into the US market and maximising long-term success.

Written by John Marcarian

John is an Australian Chartered Accountant with over 25 years of experience.

Having founded CST Tax Advisors in 1992, John has in-depth knowledge of international tax matters for both businesses and globally mobile expats.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Podcast: What A $4B Company Taught Us About Moving To Singapore

25th Jul 2026

CST Tax Advisors

Our Managing Director in Singapore, Boon Tan, recently joined Tim Raes and Jamie Bergman, hosts of the podcast Aussie Expat In the episode What A $4B Company Taught Us About Moving To...

Australian Businesses Expanding To The USA: Grants, Incentives and Support Programs

23rd Jun 2026

John Marcarian

The US Incentives Playbook: How Australian Businesses Can Turn Expansion Into Advantage For many Australian companies, the United States looks deceptively simple, one country, one flag, one...

Australian Businesses Expanding To The USA: What Legal Considerations Must Understand Before Expanding

26th May 2026

John Marcarian

The US Market Is Not One Market: What Australian Businesses Must Understand Before Expanding For Australian businesses with global ambition, the United States often represents the defining...

Expanding Stateside: A Guide to Navigating US Employment Law for Australian Businesses

John Marcarian | 17 Mar 2026 | 4 min read

Taking your Australian business to the United States is an exciting milestone, but it comes with a steep learning curve—especially regarding human resources and employment law.

In Australia, businesses rely on a familiar, centralised system governed by the Fair Work Act 2009. However, the US operates under a highly decentralised, federalist system. For Aussie expats and expanding enterprises, this means adapting to overlapping federal, state, and local regulations that can vary wildly depending on your exact location. Here is your essential guide to understanding the US labour landscape.

Navigating A Fragmented Legal Landscape

In the US, federal employment laws establish the baseline protections for workers nationwide. Statutes like the Fair Labor Standards Act (FLSA) set minimum wage and overtime rules, while the Civil Rights Act and Americans with Disabilities Act (ADA) strictly prohibit workplace discrimination.

However, federal laws are merely the floor. Individual states—and even local cities—can enact significantly stricter protections. For instance, while the federal minimum wage is set at US$7.25 per hour, states like California and New York enforce much higher minimum wages, along with enhanced paid sick leave and wrongful termination protections. Cities like San Francisco and Seattle have even more restrictive local rules. An Australian company operating in both Texas and California will face starkly different compliance landscapes, making a state-by-state HR compliance strategy absolutely essential.

The “At-Will” Culture Shock

One of the biggest paradigm shifts for Australian employers is the US at-will employment doctrine. Unlike Australia, which mandates minimum notice periods and redundancy entitlements, most US jurisdictions allow employers to terminate a worker at any time, for any reason (or no reason at all), provided the reason is not illegal.

While this flexibility allows businesses to scale their workforces rapidly, it is not an absolute rule. Crucial exceptions exist that can easily lead to wrongful termination lawsuits:

Contractual Protections – Executives or unionised workers often negotiate “just-cause” termination clauses or severance agreements.

Public Policy – You cannot fire someone for whistleblowing, refusing to commit fraud, or exercising a legal right like filing a workers’ compensation claim.

Implied Contracts – Promises made in employee handbooks or during interviews can inadvertently create implied contracts, requiring employers to follow progressive disciplinary steps before firing. To protect your business, always include clear at-will disclaimers in offer letters and handbooks, and meticulously document your reasons for any termination.

The Benefits Gap: Healthcare and Retirement

Securing top talent in the US requires understanding that employee expectations differ vastly from those in Australia.

Healthcare Is An Employer Obligation

The US lacks a universal public system like Medicare. Because access to healthcare is heavily tied to employment, offering competitive, employer-sponsored health insurance is a fundamental necessity if you want to attract and retain quality staff.

The 401(k) vs. Superannuation

Instead of compulsory 11% superannuation contributions, the US utilises a voluntary defined-contribution system known as a 401(k). Employees contribute pre-tax income, and while it isn’t legally mandated, competitive employers usually match these contributions by 3% to 6%.

Navigating Payroll Taxes And Contractor Risks

US payroll taxes are a multi-tiered system. Rather than dealing with a single entity like the ATO, employers must withhold and match Federal Insurance Contributions Act (FICA) taxes, which fund Social Security (6.2%) and Medicare (1.45%). Additionally, employers are liable for both federal and state unemployment taxes (FUTA and SUTA), with state rates fluctuating based on your specific industry and history of layoffs.

Finally, if you plan to hire freelancers, tread carefully. The IRS and Department of Labor strictly enforce worker classification laws. Misclassifying an employee as an independent contractor can trigger severe fines, back-pay claims, and lawsuits. Ensure you have well-drafted independent contractor agreements that clearly define the project scope, payment terms, and the worker’s independent status.

Conclusion

Expanding into the American market is not a one-size-fits-all endeavour. By implementing centralised HR compliance systems, understanding local legislative nuances, and consulting with US labour attorneys, Australian businesses can successfully mitigate risks and build a thriving stateside workforce.

CHECKLIST: Australia – US Market Entry Checklist

To assist you and your team we have created the “Australia-US Market Entry Checklist“. The checklist guides your team through:

Identifying the most appropriate and strategic pathways for US expansion by Australian businesses.

Reducing expansion risk through clear tax, legal, and regulatory guidance.

Enabling a smooth transition into the US market and maximising long-term success.

Written by John Marcarian

John is an Australian Chartered Accountant with over 25 years of experience.

Having founded CST Tax Advisors in 1992, John has in-depth knowledge of international tax matters for both businesses and globally mobile expats.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Podcast: What A $4B Company Taught Us About Moving To Singapore

25th Jul 2026

CST Tax Advisors

Our Managing Director in Singapore, Boon Tan, recently joined Tim Raes and Jamie Bergman, hosts of the podcast Aussie Expat In the episode What A $4B Company Taught Us About Moving To...

Australian Businesses Expanding To The USA: Grants, Incentives and Support Programs

23rd Jun 2026

John Marcarian

The US Incentives Playbook: How Australian Businesses Can Turn Expansion Into Advantage For many Australian companies, the United States looks deceptively simple, one country, one flag, one...

Australian Businesses Expanding To The USA: What Legal Considerations Must Understand Before Expanding

26th May 2026

John Marcarian

The US Market Is Not One Market: What Australian Businesses Must Understand Before Expanding For Australian businesses with global ambition, the United States often represents the defining...

Immigration And Visas: The Practical Playbook For Australian Businesses Entering The US

John Marcarian | 20 Feb 2026 | 8 min read

Expanding into the US can be a growth-defining move for an Australian business — new customers, deeper capital markets, a bigger talent pool. But there’s one reality that catches founders off guard: in the US, immigration isn’t a “formality.” It’s a regulated operating system. If you treat it like admin, it will eventually treat you like a compliance event.

At a high level, three agencies shape most employment- and investment-based pathways:

USCIS (US Citizenship and Immigration Services) – adjudicates petitions and many work-authorisation processes inside the US

DOL (Department of Labor) – protects US wage and working-condition standards (especially for employer-sponsored roles)

DOS (Department of State) – issues visas at US embassies/consulates outside the US

When these agencies don’t align — or when documentation isn’t airtight — the cost is rarely “just delay.” It can disrupt onboarding, derail projects, and create legal exposure you don’t want attached to your US launch.

The E-3 Visa: Australia’s Unfair Advantage (When You Can Use It)

For many Australian companies and professionals, the E-3 is the cleanest entry point. It’s available only to Australian citizens working in a specialty occupation (typically requiring at least a bachelor’s degree or equivalent).

Why it’s so attractive:

A dedicated annual cap (10,500) that has historically not been reached

Lower friction and cost compared to many alternatives

Renewable in two-year increments with the ability to extend repeatedly (so long as eligibility remains)

A major practical benefit: spouses of E-3 holders can obtain work authorisation (EAD) and work broadly in the US. For many families, that single feature makes the E-3 dramatically more livable than other work visas.